Saving For College

One of the major life expenses, besides retirement and buying a home, is paying for college. Unfortunately the cost of sending a child to college has increase about twice as fast as inflation, about 5%-8% a year. The College Board issued a news release that the average cost for 2007-2008 at a four-year private college is $23,712/year (up 6.3 percent from last year) and at a four-year public college is $6,185/year (up 6.6 percent from last year). Published tuition and fees can run as high as $33,000/year, however 56 percent of students at four-year schools pay less than $9,000 for tuition and fees per year. A child born today could expect to pay $355,839 for four years at a private college and $92,816 for four years at a public college (calculator).

This is a lot of money, however if you view education as an investment in your child's future the costs are reasonable. A 2007 College Board Study, Education Pays, states that

"During their working lives, typical college graduates earn over 60 percent more than typical high school graduates, and those with advanced degrees earn two to three times as much as high school graduates. Salaries are not the only form of compensation correlated with education level; college graduates are more likely than other employees to enjoy employer-provided health and pension benefits. More educated people are less likely to be unemployed and less likely to live in poverty. These economic returns make financing a college education a good investment."

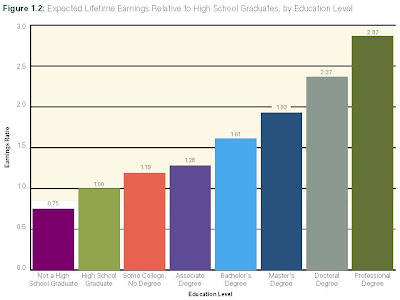

As your degree level increases, so does your total expected lifetime earnings. A master's degree (MBA,eg) is worth 93% more than a high school degree, a doctoral degree (PHD, eg) is worth 137% more, while a professional degree (MD, JD, eg) is worth 187%.

Below is a list of common ways to save for college. Each section will provide a brief summary, along with pros and cons of the methods.

Coverdell Education Savings Account

The Coverdell ESA allows you to make an annual non-deductible contribution to the savings account, which grows federally tax free. Withdrawals for qualified education expenses from the account are also tax free, in most cases. This account is similar, at least from a tax standpoint, as a Roth IRA. The money in the account can be used for accounts can be set up with most banks, brokers or mutual fund companies. This type of account lets you pay for elementary and secondary school expenses, along with other qualified education expenses.

Pros:

- Flexibility & Investment Choices - can set up ESA with most banks, brokers or mutual fund companies. You can pick your investment choices.

- Expenses - may be lower than in some state 529 plans.

- Qualified Education Expenses - include tuition (K-12 and college), fees, tutoring, books, supplies, related equipment, room and board, uniforms, transportation, extended day programs, computers, Internet access.

- Financial Aid - are treated the same as 529 Savings Plans for financial aid purposes (5.6% counted as a parent's asset).

- Transferable - funds maybe transferred to other members of your family as long as the meet the age restrictions below.

- Fees - typically are lower with this type of account.

Cons:

- Contribution Amount - a total of $2,000 a year per beneficiary.

- Earnings Restrictions - for modified adjusted gross income levels $95,000 to $110,000 (single) or $190,000 to $220,000 (married filing jointly), contributions will be limited. Over $110,000 (single) or $220,000 (married filing jointly), contributions are not allowed.

- Age Restrictions - beneficiaries must be under the age of 18 and funds must be used by 30 years old.

- Market Risk - since money is invested in stocks, bonds or mutual finds, the account could always be worth less than the contribution amount due to market risks.

529 Savings Plan

A 529 Savings Plan, or Qualified Tuition Program (QTP), works similarly to a Coverdell ESA, with some significant differences. A main difference is that these plans are set up by the states and administered by third parties, mainly mutual fund companies. In some states the contributions made to the account can be deducted from state income taxes. The plan will only cover qualified educational expenses for post-secondary education (college), but allows for higher contribution amounts

Pros:

- Taxes - possible deduction on state income taxes.

- Contribution Amount - up to $300,000 per beneficiary in many states.

- Earnings Restrictions - None to very few depending on the state.

- Age Restrictions - None to very few depending on the state.

- Financial Aid - if account is owned by parent, the assets are assessed at a maximum rate of 5.64% in determining a student's Expected Family Contribution.

Cons:

- Flexibility & Investment Choices - stuck using plans set up by the states. Most plans have limited investment choices.

- Fees - typically higher than over college savings plans.

- Taxes - can get complicated if contributions exceed the annual gift-tax exclusion of $12,000 per person.

- Market Risk - since money is invested in stocks, bonds or mutual finds, the account could always be worth less than the contribution amount due to market risks.

529 Pre-Paid Plan

A 529 Pre-Paid Plan, or Qualified Tuition Program (QTP), allows families to purchase tuition at a public college at current cost. There are two types of pre-paid plans, a contract plan and a unit plan. A contract plan lets you purchase contracts for one to five years of tuition. A unit plan let you purchase 'units' which could be equal to credit hours or a percentage of a years tuition. Contributions can be made either as a lump sum or over a period of time.

Pros:

- Market Risk - none,you are guaranteed by the state to at least match in-state tuition increases.

- Transferable - most programs allow funds to be transferred to private or out-of-state schools. You are responsible for paying the difference in tuition rates.

Cons:

- Flexibility - stuck using the state plan, geared towards state schools and often restricted to in-state residents.

- Refund/Cancellation Fees - can be required to pay high penalties to cancel plan.

- Qualified Education Expenses - limited to tuition and fees in most states.

- Financial Aid - may significantly impact the ability to secure financial aid.

UTMA/UGMA

A uniform Transfer to Minors Act or Uniform Gifts to Minors Act accounts are an account set up on behalf of a minor. The child is the owner of the account upon reaching the 'age of majority'. so they can do as they please with the money. Their plans for the money may not include college.

Pros:

- Earnings Restrictions - none.

- Flexibility & Investment Choices - can set up a UTMA/UGMA with most banks, brokers or mutual fund companies. You can pick your investment choices.

- Taxes - account is taxed at the child's income tax rate.

Cons:

- Control - Once child reaches age of majority, they control the money.

- Taxes - can get complicated if contributions exceed the annual gift-tax exclusion of $12,000 per person.

- Financial Aid - account is owned by student, the assets have a larger impact on financial aid eligibility. Could make it more difficult to secure financial aid.

- Irrevocable - money to fund to account is deemed an irrevocable gift and can not be transferred back to the parent.

- Legal - these accounts require more legal understanding than other types of accounts. This link has a good explanation of UTMA/UGMAs.

This list is not exhaustive and there are other savings methods that could be used to save for college. Most of these other are not specific to saving for education, and do not have some of the same benefits as those listed above.

Three critical points to take away from this post:

- Start Early - As with any savings goal, the earlier you start the better. There are tons of articles and studies out there illustrating this point.

- Not One Account for All - You should evaluate which account is best for you. In some cases a single type of account may not be the best

- Your Retirement - Don't short change your retirement accounts to fund your child's education. Worse case, your child has to take out student loans to attend school. In the long run paying back the loan will be cheaper than having to fund a parent's retirement.

Source

http://www.collegeboard.com/parents/csearch/know-the-options/21385.html

http://www.collegeboard.com/prod_downloads/about/news_info/trends/ed_pays_2007.pdf

http://finance.yahoo.com/college-education/article/101867/A_Crash_Course_in_College_Savings_Plans

http://www.irs.gov/publications/p970/index.html

Helpful Links

http://www.collegeboard.com/parents/pay/

http://www.finaid.org/

http://www.finaid.org/calculators/costprojector.phtml

No comments:

Post a Comment